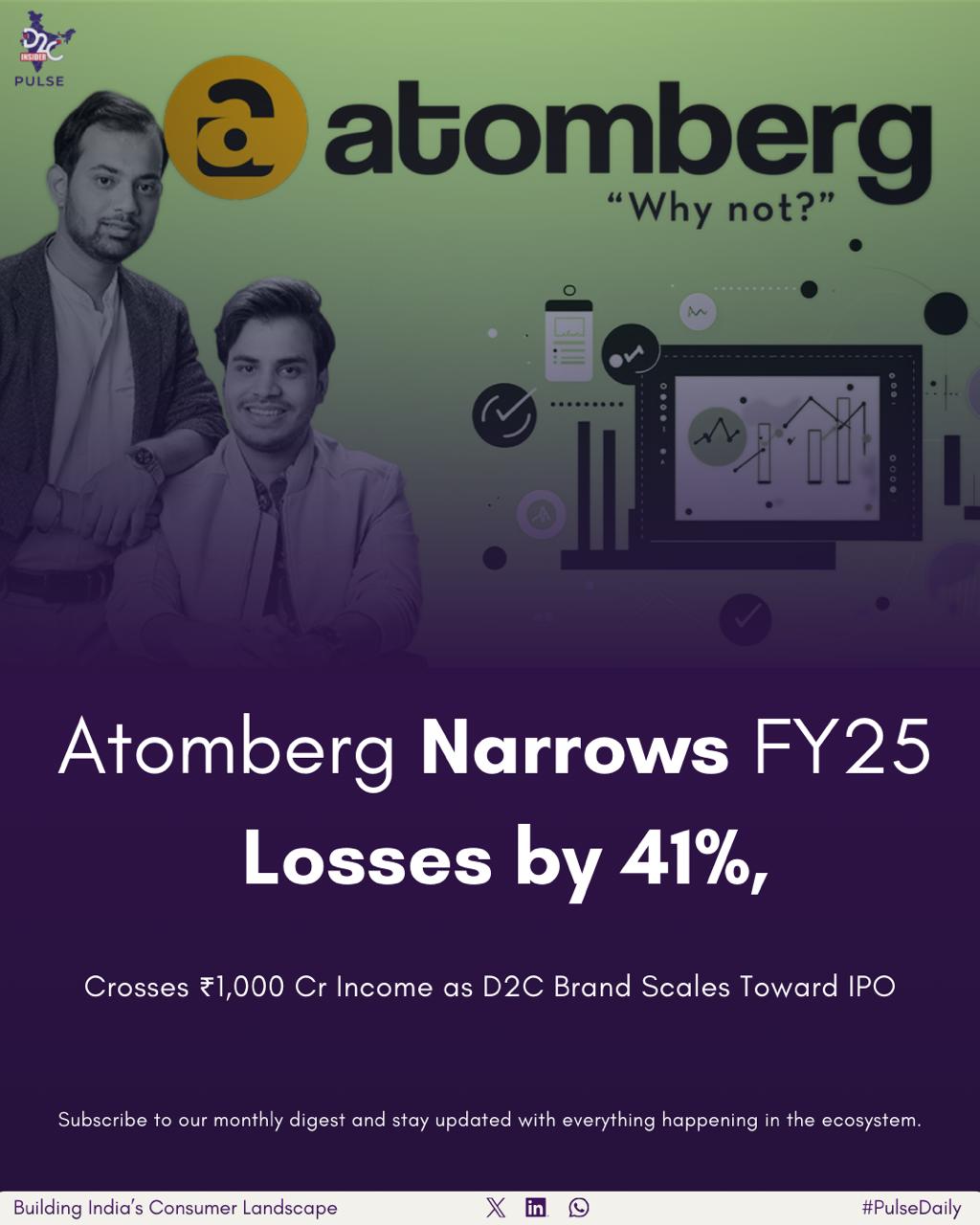

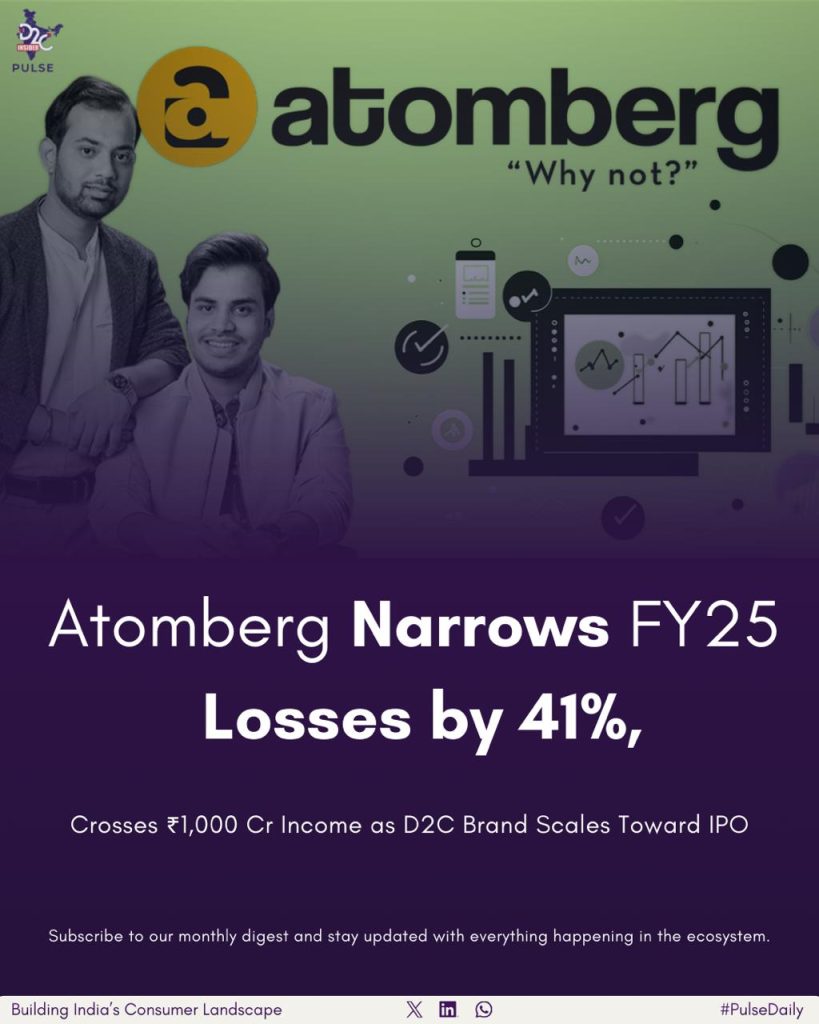

India’s D2C ecosystem continues to produce scaled consumer hardware brands with strong fundamentals, and Atomberg stands out as one of the most compelling examples. In FY25, the home appliances startup delivered a sharp improvement in financial performance, narrowing its consolidated net loss by 41 percent to ₹117.4 crore, compared to ₹199 crore in FY24, driven by strong revenue growth, disciplined cost management, and improving margins.

Atomberg’s operating revenue grew over 20 percent year-on-year to ₹958.4 crore in FY25, up from ₹797 crore in the previous fiscal. Including other income of ₹42.45 crore—earned through interest on investments, sale of investments, subsidiary income, and income tax refunds—the company’s total income crossed the ₹1,000 crore milestone, reaching ₹1,000.9 crore versus ₹825.9 crore in FY24. This marks a major scale inflection for the D2C electronics and appliances brand.

Founded in 2012 by IIT Bombay alumni Manjoj Meena and Sibabrata Das, Atomberg began as a B2B-focused energy solutions company before entering the consumer space in 2016. Its early bet on energy-efficient BLDC fan technology proved prescient, allowing the brand to establish category leadership while aligning with India’s power-efficiency narrative. Over time, Atomberg expanded its portfolio to include mixer grinders, water purifiers, smart locks, and other smart home appliances, strengthening its position within India’s fast-growing D2C electronics and gadgets segment.

A key driver of Atomberg’s growth has been its omnichannel D2C business model. The brand sells directly through its own website, leading e-commerce platforms such as Amazon and Flipkart, and an expanding offline retail network. This blended approach has helped Atomberg scale reach while maintaining brand control—an increasingly preferred strategy across D2C brands India as customer acquisition dynamics evolve.

From a cost perspective, FY25 reflected improved operational discipline. Atomberg’s total expenditure rose only 9 percent year-on-year to ₹1,118.3 crore, significantly slower than revenue growth. Cost of materials consumed remained the largest expense head, increasing modestly by 4 percent to ₹506.16 crore from ₹484.9 crore in FY24, reflecting stable procurement efficiencies despite higher volumes. Notably, employee benefit expenses declined sharply by 36.1 percent to ₹158.6 crore from ₹248.3 crore, materially contributing to margin improvement.

At the same time, Atomberg continued to invest in brand visibility. Advertising and promotional expenses rose 36 percent to ₹104 crore in FY25 from ₹76.42 crore in FY24, underscoring a continued focus on strengthening consumer recall and brand leadership in an increasingly competitive D2C appliance market.

On the funding front, Atomberg remains well-capitalised. The company has raised approximately $126.5 million to date from marquee investors including Temasek Holdings, Steadview Capital, A91 Partners, Jungle Ventures, Inflexor Ventures, and others. More recently, Atomberg has been in discussions to raise $4.8 million (₹40 crore) in secondary capital in a round led by Forj Capital, with participation from White Whale Partners and prominent angel investors including Tanmay Bhatt—highlighting continued investor confidence in the brand’s trajectory.

Looking ahead, Atomberg is preparing for a $200 million IPO and is targeting a public listing in FY27. With revenue nearing ₹1,000 crore, losses narrowing rapidly, and strong brand equity across India’s D2C ecosystem, the company appears well-positioned to transition from a high-growth private brand to a publicly listed consumer electronics leader.

Within the broader D2C industry news cycle, Atomberg’s FY25 performance reinforces a larger trend: scaled D2C hardware brands that combine product innovation, omnichannel distribution, and cost discipline are emerging as long-term category leaders. As India’s demand for energy-efficient, smart home appliances continues to rise, Atomberg’s journey reflects the maturity and ambition of the next generation of Indian D2C businesses.