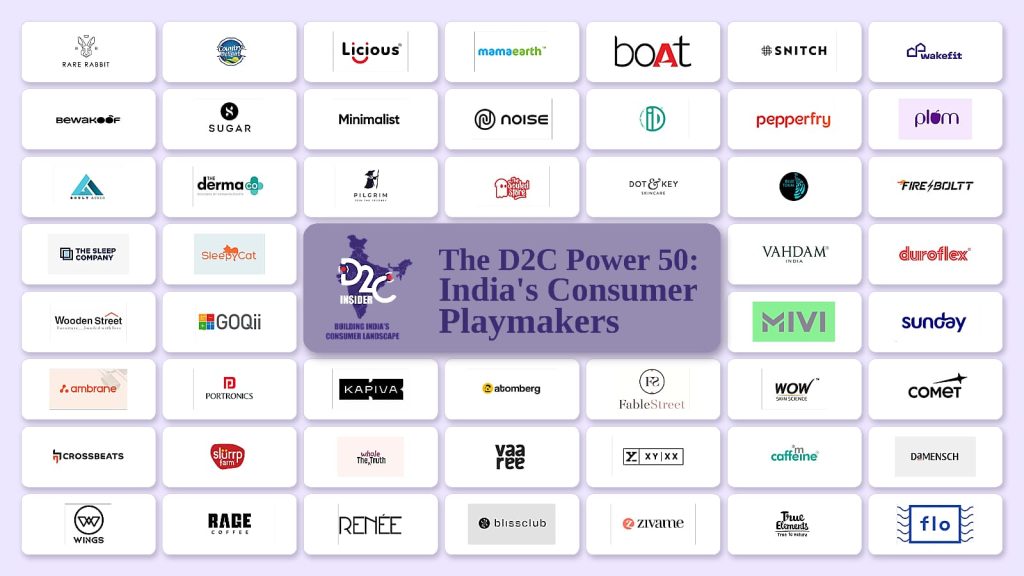

India’s direct-to-consumer economy has moved past its discount-and-Instagram-ads phase. The brands that matter now are the ones that paired a genuine product insight with founder conviction, then built the supply chain, retail footprint, and unit economics to back it up. Here are 50 of them, across the five categories driving the space today.

A note on the ranking: Brands within each category are ordered by relative scale — a blend of disclosed/audited revenue, total funding raised, valuation, and parent-company backing, weighted in that priority order wherever more than one signal exists. This is a directional ranking, not a precise one. A handful of these brands (Wakefit, Honasa/Mamaearth) are publicly listed with audited financials; most are private, and their numbers are self-reported, press-estimated, or inferred from funding rounds. Each entry is tagged with the primary basis used to rank it, so you can weigh confidence yourself rather than take the order as gospel.

1. Apparel, Footwear & Fashion

1. Rare Rabbit

Founded in 2015 by husband-wife duo Manish and Akshika Poddar, Rare Rabbit grew out of their family’s export-manufacturing business, Radhamani Textiles, which once supplied Zara’s parent Inditex. The brand bet on premium men’s smart-casual wear — quirky prints, playful product names, and no permanent discounting — at a time when most competitors chased volume through sales. It paid off: revenue crossed ₹637 crore in FY24, up 69% year-on-year, with profit more than doubling to ₹75 crore, and later reporting points to revenue nearing ₹700 crore with profit close to doubling again. Today Rare Rabbit runs 150+ stores across metros and tier-2/3 India, has closed a ₹500 crore institutional round led by A91 Partners, and is widely expected to cross the ₹1,000 crore mark under The House of Rare umbrella. Scale basis: audited revenue (RoC filings via Tofler/Entrackr) — highest verified revenue in this category.

2. Bewakoof

Founded in 2012 by Prabhkiran Singh and Siddharth Munot, Bewakoof (literally “fool” in Hindi) built its brand on quirky, meme-driven, mass-accessible fashion for India’s 16–34 demographic, growing early traction through Facebook and college campus giveaways. Its differentiation was cultural relatability over premium positioning. Bewakoof was acquired into Aditya Birla Group’s D2C arm, TMRW, giving it access to serious retail and manufacturing muscle. In 2026 the brand is focused on restructuring its unit economics and lowering customer acquisition costs under Birla’s backing, while staying anchored to youth casualwear and graphic tees. Scale basis: parent-company backing (Aditya Birla Group/TMRW) — exact standalone revenue not independently disclosed.

3. The Souled Store

Founded in 2013 by Aditya Sharma, Harsh Lal, Rohin Samtaney, and Vedang Patel, The Souled Store built India’s largest pop-culture merchandising business by licensing Marvel, DC, anime, and sports IP onto everyday casualwear. Its differentiation is fandom-first design paired with genuine community engagement. The brand has stayed profitable while scaling, with ARR reportedly tracking toward ₹600 crore, expanding from licensed merchandise into broader casualwear with a growing offline store network in destination malls. Scale basis: press-reported revenue estimate (unaudited) — widely cited but not independently confirmed.

4. Snitch

Founded in 2018 by Siddharth Dungarwal, Snitch built its identity on speed — weekly style drops for young Indian men, backed by an automated, trend-responsive supply chain rather than seasonal collections. Often described as “the Zara of India,” Snitch leaned hard into Shark Tank India visibility and influencer-led marketing. It’s now expanding aggressively into physical retail across tier-1 and tier-2 cities, with reported revenue in the ₹400–500 crore range, while keeping its digital-first, high-frequency product cadence as its core edge. Scale basis: press-reported revenue estimate (unaudited).

5. Zivame

Founded by Richa Kar, Zivame was one of India’s earliest attempts to normalize online intimate-apparel shopping in a market where women often avoided in-store bra fittings altogether. Its differentiation was a profile-based size-recommendation engine and detailed fit education content. Zivame has since gone through ownership changes (including Reliance Retail’s backing) and structural adjustments, but remains a category leader with strong online volume, backed by physical consultation studios — a hybrid model few intimatewear competitors have matched. Scale basis: parent-company backing (Reliance Retail) — standalone financials not disclosed.

6. XYXX

Founded in 2017 by Yogesh Kabra along with Siddhartha Gondal, XYXX Crew set out to modernize men’s innerwear and loungewear with fabric innovation — Lenzing MicroModal and bamboo-cotton blends, seamless construction, and performance-grade elastic. Rather than compete purely online, XYXX pushed hard into offline distribution, now present in over 20,000 multi-brand outlets. Revenue grew from ₹131 crore in FY24 to roughly ₹192 crore in FY25, and the brand — backed by investors including KL Rahul — continues expanding its loungewear and athleisure lines. Scale basis: audited revenue (RoC filings) — smaller than Rare Rabbit but among the most reliably verified figures here.

7. DaMENSCH

Founded in 2018 by Anurag Saboo and Gaurav Pushkar, DaMENSCH focuses on premium men’s essentials built around “slow-fashion tech” designed to resist color fade and shrinkage over repeated washes. Backed by A91 Partners, Matrix Partners, and others with over $24 million raised, DaMENSCH grew revenue over 22% to ₹72+ crore in FY23 and competes directly with XYXX and legacy players like Dollar Industries, continuing to expand its innerwear and loungewear catalog. Scale basis: audited revenue (RoC filings).

8. BlissClub

Founded in 2020 by Minu Margeret, a former Myntra and Zivame executive, BlissClub set out to build technical activewear engineered for Indian women’s body types, shaped by direct community feedback loops. Backed by investors including Elevation Capital and Mamaearth’s Ghazal Alagh, BlissClub grew revenue from ₹15 crore to ₹68 crore in a single year (FY23). It’s now scaling through its own exclusive brand outlets in major metros. Scale basis: audited revenue (RoC filings) — smallest verified revenue in this category, but fastest disclosed growth rate.

9. FableStreet (FS Life)

Founded in 2016 by Ayushi Gudwani, FableStreet set out to solve tailoring for Indian professional women — Western workwear cut specifically for Indian proportions. The brand has since expanded into a multi-label house under FS Life, adding Mikoto and March. It continues to scale primarily in corporate and metro hubs, positioning itself as a specialist in a niche larger fast-fashion players have largely ignored. Scale basis: press mentions/market position — no revenue or funding figure independently verified; ranked here on niche market presence alone.

10. Comet

Founded in 2023 by Utkarsh Gupta and Dishant Daryani — two ex-consultants (Hotstar, Urban Company) who bonded over sneaker culture — Comet set out to fill a gap between ₹2,000 budget sneakers and ₹10,000+ global brands with culturally-rooted limited drops sold at a “mass-premium” ₹4,000–5,000 price point. Backed by Elevation Capital and Nexus Venture Partners with over $6.5 million raised, Comet hit a reported ₹167 crore valuation within two years and is now opening its first high-street stores in Bengaluru, Delhi, and Mumbai. Scale basis: funding/valuation — youngest brand in this category, smallest current revenue (reportedly ₹4–5 crore in monthly sales), but included for trajectory and investor backing.

2. Beauty & Personal Care

1. Mamaearth (Honasa Consumer)

Founded in 2016 by Varun and Ghazal Alagh, Mamaearth built its identity around toxin-free, natural-ingredient personal care — becoming India’s first D2C beauty unicorn on the strength of that transparency positioning. Parent company Honasa Consumer went public and now operates a portfolio of brands beyond Mamaearth, including The Derma Co. Despite intensifying competition, Mamaearth remains the flagship, leaning on its wide product range and deep offline retail penetration. Scale basis: audited revenue (publicly listed parent company) — the only fully audited, publicly disclosed figure in this category.

2. The Derma Co

Part of the Honasa Consumer stable, The Derma Co was built to bridge casual skincare and dermatologist-grade treatment — clinical, concern-specific formulations backed by AI-assisted dermatological consultations. Riding Honasa’s distribution and marketing infrastructure, The Derma Co has become one of the fastest-scaling brands in the group’s portfolio, reportedly crossing ₹500 crore in quarterly run-rate territory, and continues to expand its acne, sunscreen, and moisturizer lines. Scale basis: parent-company disclosure (Honasa quarterly reporting) — strong signal, though “quarterly run-rate” isn’t the same as audited annual revenue.

3. Sugar Cosmetics

Founded by Vineeta Singh and Kaushik Mukherjee, Sugar Cosmetics carved out color cosmetics for Indian skin tones and tropical heat. Sugar has matured into one of the most balanced omnichannel beauty players in the country, splitting revenue roughly evenly between online and its thousands of offline retail touchpoints — a structural maturity most D2C beauty brands haven’t reached. Scale basis: market position and offline footprint — widely regarded as top-3 by scale, but standalone audited revenue wasn’t confirmed in my research.

4. Plum Goodness

Founded by Shankar Prasad, Plum built its identity as a 100% vegan, PETA-certified “clean beauty” label years before clean beauty became mainstream in India. Plum has grown into a nationally distributed cross-category player spanning skincare, haircare, and color cosmetics, with a reported revenue run-rate around ₹350 crore in FY24. Scale basis: press-reported revenue estimate.

5. Dot & Key

Now majority-owned by Nykaa, Dot & Key built its differentiation on “fruit-forward,” visually engaging skincare formulations. Since Nykaa’s acquisition, the brand has become a significant growth driver within Nykaa’s house-brand portfolio, leaning heavily on quick-commerce distribution to capture impulse skincare purchases. Scale basis: parent-company backing (Nykaa, publicly listed) — standalone revenue not separately disclosed.

6. Minimalist

Founded by brothers Mohit and Rahul Yadav, Minimalist built its brand on percentage-disclosed, science-backed actives. Minimalist has scaled into one of India’s most credible clinical-skincare names, holding strong margins domestically while pushing export growth into the Middle East, Southeast Asia, and Western markets — an unusually international trajectory for an Indian D2C skincare brand. Scale basis: institutional backing signal — reported to have drawn investment interest from a major FMCG player, though I could not independently confirm deal specifics; treat this ranking as provisional.

7. Pilgrim

Founded in 2019 by Anurag Kedia and Gagan Deep Makker, Pilgrim’s differentiation is importing “global beauty secrets” and reformulating them for Indian skin and hair. Pilgrim has raised roughly $56 million to date, including a ₹200 crore round in 2025 at a pre-money valuation of about ₹3,000 crore, and crossed ₹200 crore in revenue by FY24. Scale basis: audited-adjacent revenue + disclosed valuation — among the more reliably sourced figures in this category.

8. Wow Skin Science

Built around natural, chemical-free actives — apple cider vinegar, onion oil, and botanical extracts. As domestic competition intensified, Wow has increasingly leaned on international marketplace sales (notably Amazon US) to sustain growth, while continuing to reinforce its haircare and wellness lines domestically. Scale basis: market longevity and international presence — no recent revenue figure verified.

9. Renée Cosmetics

Founded by Ashutosh Valani, Priyank Shah, and actor Aashka Goradia, Renée focuses on color cosmetics built around accessible, impulse-buy price points. Backed by $54 million in funding across six rounds (including a Series C in August 2025), Renée has scaled aggressively through 2025–26, expanding its SKU range and distribution. Scale basis: disclosed funding total ($54.3M) — solid signal, but revenue not independently confirmed.

10. mCaffeine

Founded in January 2016 by Tarun Sharma and Vikas Lachhwani, mCaffeine carved out a niche in caffeine-infused personal care. The brand crossed ₹100 crore in revenue within four years and has since pushed hard into offline retail (now roughly a third of sales, with over 5,000 stores), targeting a ₹1,000 crore revenue milestone. Scale basis: press-reported historical revenue (₹100 Cr as of ~2020) — smallest confirmed current scale in this category, though targets suggest faster growth ahead.

3. Food & Beverages

1. Licious

Founded by Abhay Hanjura and Vivek Gupta, Licious tackled one of Indian retail’s biggest trust gaps: hygienic, traceable meat and seafood. Licious became India’s first D2C unicorn, has raised roughly $490 million in total funding to date, and has since expanded into ready-to-eat and plant-based ranges (via its Uncrave label). The company is now reportedly targeting a roughly $2 billion valuation ahead of a planned 2026 IPO. Scale basis: disclosed total funding (~$490M) and unicorn/IPO-track status — highest funding total in this category.

2. Country Delight

Founded in 2015 by Chakradhar Gade and Nitin Kaushal, Country Delight set out to fix a broken supply chain: unadulterated milk delivered fresh, with full traceability back to the farm, on a subscription model. The company has raised over $220 million to date and expanded well beyond milk into eggs, ghee, fruits, and household staples — India’s largest fresh-supply D2C business by scale. Scale basis: disclosed total funding (~$221M) and category-leading subscriber volume.

3. iD Fresh Food

Founded by PC Musthafa along with his cousins, iD Fresh Food modernized fresh idli and dosa batter — preservative-free, consistently available, and nationally distributed. iD Fresh has since expanded into parotas, dairy, and other ready-to-cook staples, building genuinely massive regional and national distribution built on daily-use consistency. Scale basis: market position and distribution footprint — long-established, bootstrap-to-scale story; specific current revenue not independently confirmed here.

4. The Whole Truth

Founded by Shashank Mehta, The Whole Truth built its brand around declaring 100% of ingredients on the front of the pack, with zero added sugar and zero preservatives. Heavily backed by institutional capital, The Whole Truth has become the clean-label benchmark other snack brands are now measured against. Scale basis: institutional funding backing — specific amount and revenue not independently confirmed here.

5. True Elements

Founded by Sreejith Moolayil and Puru Gupta, True Elements built its identity on certified 100% whole-grain, zero-sugar-coated breakfast products. The company was acquired into Marico’s portfolio, giving it access to serious distribution and manufacturing infrastructure most standalone D2C snack brands lack. Scale basis: parent-company backing (Marico, publicly listed) — a meaningful scale signal even without standalone revenue disclosure.

6. Blue Tokai Coffee Roasters

Founded by Matt Chitharanjan and Namrata Asthana, Blue Tokai set out to build specialty coffee culture in India from the source up. Its hybrid model — online bean subscriptions feeding a growing café network — lets the brand capture both high-margin retail and experiential café revenue, with continued café footprint expansion in major cities. Scale basis: market position and multi-city café footprint — funding and revenue figures not independently confirmed here.

7. Vahdam India

Founded by Bala Sarda, Vahdam set out to sell India’s tea heritage directly to global consumers — single-origin, estate-fresh teas packaged at source and shipped internationally. Vahdam has built a genuinely high-margin, export-oriented business selling into international luxury retail channels while maintaining domestic availability. Scale basis: export/international market position — an unusually outward-facing model, but specific revenue not independently confirmed here.

8. Kapiva

Founded by Ameve Sharma, Kapiva set out to make Ayurvedic nutrition genuinely convenient — juices, capsules, and health gummies formatted for modern routines. The brand has captured meaningful ground in India’s broader wellness boom by targeting time-strapped urban professionals. Scale basis: market position within wellness category — no funding or revenue figure independently confirmed here.

9. Slurrp Farm

Founded by Meghana Narayan and Shauravi Malik, Slurrp Farm built its business around millet-based, zero-refined-sugar, zero-maida snacks for toddlers and young children, staying tightly connected to a community of mothers from day one. The brand has become a dominant force in India’s healthy children’s nutrition category. Scale basis: category leadership in a defined niche — smaller addressable market than the general snacking brands above it.

10. Rage Coffee

Founded by Bharat Sethi, Rage Coffee targeted instant coffee for younger, energy-seeking consumers, fortified with vitamins and higher caffeine content. Rage has leaned heavily into rapid quick-commerce channels to capture impulse purchases, continuing to expand its flavored and functional coffee range. Scale basis: market position — newest positioning among this group, no funding or revenue figure independently confirmed here.

4. Consumer Electronics & Smart Wearables

1. boAt Lifestyle

Founded in 2016 by Aman Gupta and Sameer Mehta, boAt built India’s biggest audio and wearables brand combining aggressive, celebrity-backed branding with prices far below Apple and Sony. boAt is a unicorn and, despite a roughly 5% revenue dip to about ₹3,100 crore in FY25 from ₹3,285 crore in FY24, remains far larger than any other brand in this category by disclosed revenue, with an IPO widely discussed. Scale basis: audited/disclosed revenue — by far the largest verified figure in this category.

2. Noise

Founded in 2014 by brothers Amit and Gaurav Khatri, Noise started by selling phone cases before pivoting into affordable smartwatches and wearables. Noise has consistently ranked among India’s top smartwatch brands by unit volume and continues to push feature-rich fitness and connected-device ecosystems. Scale basis: market position (top smartwatch brand by volume) — revenue not independently confirmed here.

3. Fire-Boltt

Co-founded by Arnav Kishore, Fire-Boltt built its business around feature-rich smartwatches at aggressive price points designed to match pricier competitors’ spec sheets. Fire-Boltt has rapidly become one of India’s top-selling smartwatch brands by volume, competing directly with boAt and Noise. Scale basis: market position (top-3 smartwatch brand by volume) — revenue not independently confirmed here.

4. Boult Audio

Founded by brothers Varun and Tarun Gupta, Boult entered the audio market through Myntra with entry-level neckbands before expanding into smartwatches and true wireless earbuds. Boult posted the highest year-on-year growth in TWS shipments among major Indian players in a recent tracked quarter, outpacing established rivals. Scale basis: market share growth data (IDC-tracked shipment share) — a real but narrower metric than total revenue.

5. Ambrane India

Founded in 2012 by brothers Ashok and Sanjay Rajpal, Ambrane spotted the power bank opportunity early, building its own Haryana manufacturing facility in 2014 well ahead of India’s broader “Make in India” push. The company has stated a target of crossing ₹500 crore in revenue, and continues to expand its charging ecosystem products. Scale basis: self-disclosed revenue target and manufacturing scale — historical reported turnover was ₹115 crore some years ago, with stated ambition toward ₹500 crore; treat the higher figure as a target, not a confirmed current number.

6. Mivi

Founded in 2016 by husband-and-wife duo Viswanadh Kandula and Midhula Devabhaktuni, Mivi built its own “Make in India” production facility in Hyderabad in 2021 and has stayed bootstrapped and profitable since day one — a genuinely differentiated financial discipline in a category most competitors have funded through losses. Scale basis: market position and manufacturing scale — smaller than the majors above by revenue, but notable for profitability without external funding.

7. GOQii

Founded by Vishal Gondal, GOQii paired fitness tracking devices with a human health-coaching platform, positioning itself as a preventative healthcare platform rather than a pure gadget brand. It continues to expand its health-insurance-linked tracking programs for preventive-care-focused consumers. Scale basis: market position in a differentiated niche (wellness platform, not pure hardware) — revenue and funding not independently confirmed here.

8. Portronics

Founded in 2010 by Jasmeet Singh, Portronics built its business around practical, inventive gadgets — desktop accessories, car chargers, portable speakers — sold through both e-commerce and offline partners like Reliance Digital and Croma, with 200+ retail touchpoints. Scale basis: retail footprint (200+ touchpoints) — revenue not independently confirmed here.

9. Crossbeats

Crossbeats has positioned itself in the mid-to-high premium segment of D2C watches and audio, emphasizing AMOLED displays and metal-alloy builds rather than competing purely on entry-level pricing. Scale basis: market positioning only — no revenue or funding figure independently confirmed here; ranked near the bottom on scale by default.

10. Wings

Wings carved out a specific niche within India’s audio market: gaming-focused earbuds and peripherals, built around ultra-low-latency audio for India’s mobile gaming audience — a deliberately narrow focus compared to the broader-catalog players above it. Scale basis: market positioning in a narrow niche — no revenue or funding figure independently confirmed here.

5. Home Decor, Furnishings & Sleep Tech

1. Wakefit

Founded in 2016 by Ankit Garg and Chaitanya Ramalingegowda, Wakefit set out to fix India’s fragmented, low-trust mattress retail market with direct-to-consumer memory foam mattresses backed by a 100-night trial and 10-year warranty. Wakefit went public in December 2025 (Wakefit Innovations Ltd), raising ₹1,288.89 crore in a listing that valued the company at roughly ₹6,340 crore; the stock has since traded down to a market cap in the ₹4,000–4,100 crore range. FY25 revenue rose 28% to ₹1,305 crore from ₹1,017 crore in FY24, and the company turned profitable in the first half of FY26. Scale basis: audited revenue (publicly listed) — the only fully audited figure in this category and the clear largest.

2. Pepperfry

Founded in 2012 by Ambareesh Murty and Ashish Shah, Pepperfry started as one of India’s earliest online furniture marketplaces before evolving into a full destination for furniture and home decor, combining digital convenience with physical “experience studios.” It remains one of the longest-established, largest-assortment players in this category. Scale basis: market longevity and assortment breadth — one of the oldest and most recognized players; standalone current revenue not independently confirmed here.

3. Duroflex

A legacy Indian mattress and sleep-solutions manufacturer that has modernized to compete with newer D2C entrants, Duroflex differentiates itself through decades of orthopedic and spinal-support research and manufacturing scale that younger challenger brands haven’t yet built, now adopting D2C-style direct sales alongside its traditional retail base. Scale basis: legacy manufacturing scale — a long-established manufacturer with retail distribution predating the D2C wave; exact current revenue not independently confirmed here.

4. The Sleep Company

Founded by Priyanka and Harshil Salot, The Sleep Company built its differentiation around patented SmartGRID technology, positioning itself as the science-led challenger to Wakefit’s scale story. The brand continues to grow at healthy double-digit margins and has expanded from mattresses into smart recliners and ergonomic office seating. Scale basis: market position as the most-cited “challenger” brand — funding and revenue not independently confirmed here.

5. Wooden Street

Wooden Street built a large-scale, tech-enabled custom furniture platform centered on solid wood construction, backed by extensive brick-and-mortar display studios where customers can inspect craftsmanship before ordering. Scale basis: retail footprint (extensive studio network) — revenue not independently confirmed here.

6. Atomberg Technologies

Founded by IIT Bombay alumni Manoj Meena and Sibabrata Das, Atomberg tackled energy-efficient home appliances, starting with Brushless DC (BLDC) motor ceiling fans. Atomberg has closed substantial institutional funding rounds and continues to face pricing pressure as legacy fan brands roll out competing BLDC ranges. Scale basis: disclosed institutional funding — specific amount not independently confirmed here, but multiple rounds closed.

7. Vaaree

Vaaree evolved from a curated home-decor marketplace into an in-house D2C label, focused on factory-to-home sourcing of soft furnishings and kitchenware. Its differentiation is curation velocity in a category increasingly driven by social-media-led design trends. Scale basis: market positioning only — no revenue or funding figure independently confirmed here.

8. SleepyCat

SleepyCat pioneered India’s “mattress-in-a-box” delivery format well before it became a standard industry approach, giving it early-mover credibility. It now positions slightly upmarket from Wakefit’s value-led approach, competing for design-forward, boutique-brand buyers. Scale basis: early-mover positioning — likely smaller current scale than Wakefit or The Sleep Company; revenue not independently confirmed here.

9. Sunday Mattresses

Sunday Mattresses has positioned itself as a niche premium sleep brand built around organic latex and internationally certified, allergy-free raw materials, competing for a smaller but higher-margin segment of buyers. Scale basis: niche premium positioning — smallest addressable segment in this category by design; no revenue or funding figure independently confirmed here.

10. Flo Mattress

Flo Mattress built its identity as a digital-first sleep brand aimed at young professionals, using foam formulated to mitigate body-heat retention in India’s hot, humid climate. It focuses on affordability and comfort-engineering rather than premium positioning. Scale basis: market positioning only — no revenue or funding figure independently confirmed here.